What makes this piece of paper “money”? That is a thing I’ve always wondered about, and you probably have as well. To be honest, anything can be money and there have been many different types of money throughout history.

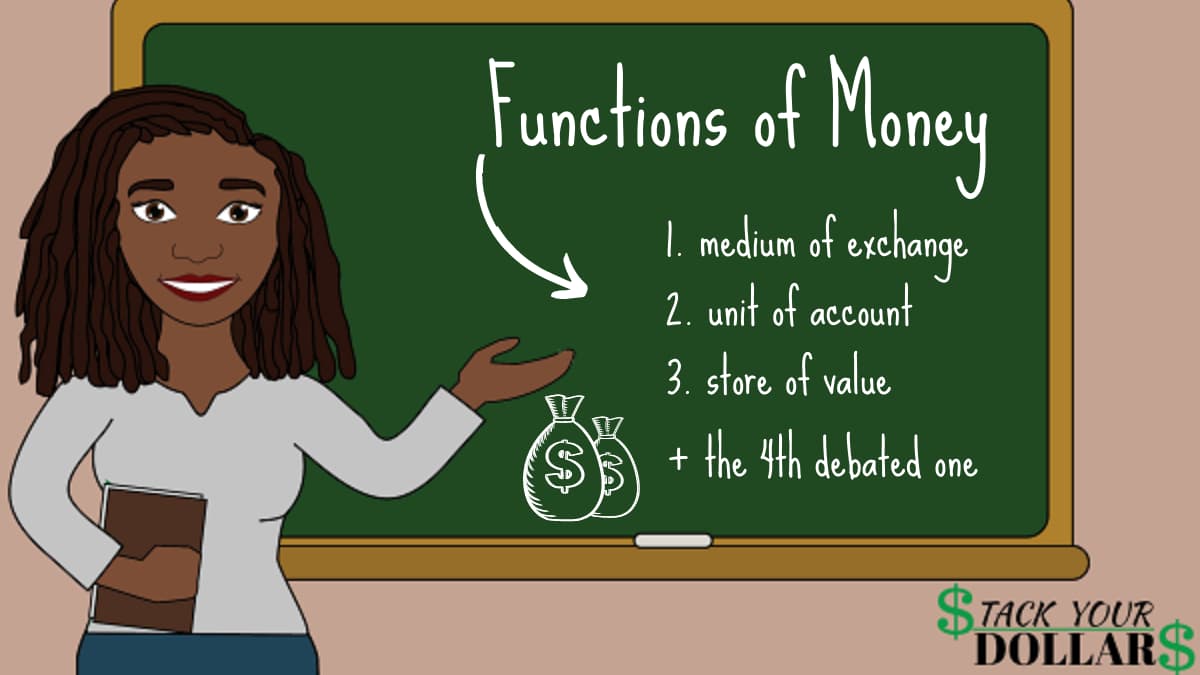

For money to be considered as such, it must be generally accepted and serve 3 functions of money (medium of exchange, unit of account & store of value).

Money is defined by the three functions (or services) that it provides:

1. A Medium of Exchange

Serving as a medium of exchange is the most important function of money. It must be widely accepted as a form of payment in the exchange for goods and services.

Before money, people would have to barter to get the things that they need. Bartering is like trading or swapping. To get something you would have to give something in return.

For example: Let’s say you wanted to buy a bag of sugar and only had a pair of slippers to trade. You would have to hope that person needed slippers or you wouldn’t get the sugar.

When both parties have an item that the other wants, this is called a double coincidence of wants. This is good because it would make a successful barter.

However, that is the downfall of bartering due to every item not being accepted as a form of payment. Therefore, things that are called “money” function as a medium of exchange that everyone accepts.

2. Unit of Account

Functioning as a unit of account, money is a common standard for measuring the value of goods and services. It’s generally consistent and allows you to know how much an item is worth.

Let’s use U.S. dollars as an example. People generally accept that a bottle of water is worth 1 dollar bill, or $1. If one was charged 35 dollar bills, $35, for a bottle of water, that would be outrageous.

However, what if you were charged 5 apples for a bottle of water, how would you know if that’s a fair deal or not?

It’s easier to know prices and their worth when money is used as a common measure.

3. Store of Value

As a store of value, money must retain its worth over time. It should be able to be saved, stored, and retrieved while still being a reliable medium of exchange.

For instance, using produce as money would not work because it does not retain its value. Why?

Let’s say that you sell your house for 100,000 tomatoes. After a few days, you’ve probably used 4 tomatoes, and the rest are spoiled. Tomatoes don’t last long so you can’t use them to buy anything else now. They do not maintain value.

On the other hand, one could say that the money we use today does not actually “store value” either due to inflation/deflation. But that’s a discussion for another day!

4. Standard of Deferred Payment

Depending on which economist you ask, there are actually 4 functions of money with the 4th being a standard of deferred payment. However, others would argue that it can be grouped under the other three.

A standard of deferred payment means that it is a widely accepted way to value and repay debt. It is a way to acquire goods and services today with the promise of repaying them at a later date.

I would also argue that it is not truly a fourth function due to it needing to serve as the first 3 in order to repay debts. It must be:

- a unit of exchange accepted

- a unit of account to measure the worth of the good or service to be repaid

- and a store of value in order to still be a fair trade years later (but still affected by inflation/deflation)

Now that you’ve learned more bout money… What is your opinion on this matter?