Today, I want to shine a spotlight on a mighty piece of legislation that stands tall in the realm of military benefits—the Servicemembers Civil Relief Act (SCRA).

Now, I know what you’re thinking, “SCRA? Is that some fancy naval term?” Well, not quite, but it does provide a lifeline of protections and benefits for our brave servicemembers.

So, grab your life jackets and join me as we delve into the depths of the SCRA. If you’re drowning in debt, high-interest rates, or need help navigating the choppy waters of legal and financial challenges, the SCRA benefit can help!

This post may contain affiliate links as a way to support the costs of this website (at no additional cost to you); however, I won’t recommend products I don’t believe in. View my full disclosure at the bottom of the page.

What is the SCRA Act?

“The Servicemembers Civil Relief Act (SCRA) provides many protections for service members and their families. “It covers issues such as rental agreements, security deposits, prepaid rent, evictions, installment contracts, credit card interest rates, mortgage interest rates, mortgage foreclosures, civil judicial proceedings, automobile leases, life insurance, health insurance and income tax payments.” – Department of Justice

This law was enacted in 2003 as a way to relieve the financial stressors on servicemembers of the United States so that they can devote their energy to their military service.

Here are some key provisions and protections offered by the SCRA:

- Interest rate cap

- Protection against eviction

- Delay of civil proceedings

- Termination of contracts

- Protection against repossession

Who is eligible for SCRA benefits?

The SCRA benefit covers full-time Active duty members, Reservists, and National Guard members while on active duty. It also provides certain benefits and protections to dependents.

SCRA Interest Rate Cap

Let’s dive a little more into what the interest rate cap means. Well, one such benefit of the SCRA is getting a cap of a 6% interest rate on financial obligations (i.e. loans, credit cards) taken out by the service member PRIOR to joining the military.

“The creditor must forgive this interest retroactively.” – U.S. Department of Justice

When you apply for the SCRA benefit at the financial institute you are with, if eligible, they’ll send you a refund with the difference of the interest you’ve paid above that 6%.

For example, if you purchased a car before entering the military with an interest rate of 20%, it will lower your rate to 6%. Then you will get back all that money you paid.

Among others, these are some of the financial obligations that are eligible for the 6 percent interest rate benefit:

- Credit cards

- Automobile, ATV, boat and other vehicle loans

- Mortgages

- Home equity loans

- Student loans

Now, I wasn’t eligible to get this myself because I didn’t use credit cards until recently; however, I have seen many testimonies from others. I have seen people who have gotten checks with thousands of dollars back (and I am not in the least bit exaggerating).

Their refunds have been so large that their remaining debt was completely paid off and then they still received extra money to pocket after that.

What I have also seen is:

- People getting refunds from accounts that have been closed for years.

- Some financial institutions will also apply it to accounts opened AFTER the service member joined the military.

- There are also those that will extend this benefit to the spouse without the service member being a joint member on the account.

How to apply for SCRA benefits

Applying for this is quite simple but might differ a bit depending on the lender. All you should have to do is:

- Send in a written request with the account number, service member’s name, active duty start date, and social security number.

- Attach a copy of their current orders that includes their active duty start date.

Simple, right? So try it! Try it everywhere!

Credit cards. Mortgages. Car loans. EVERYWHERE. Even Sallie Mae and Navient do this. So try those and other student loans. What does it hurt for the chance of getting so much money back?

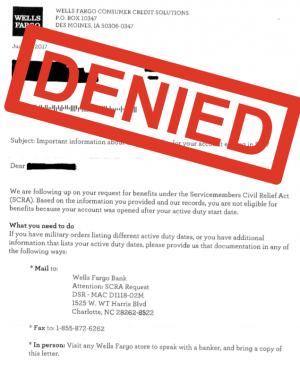

The worst you can get is a letter of rejection like I did.